3 min read

Scientist Discovered Why Most Traders Lose Money – 24 Surprising Statistics

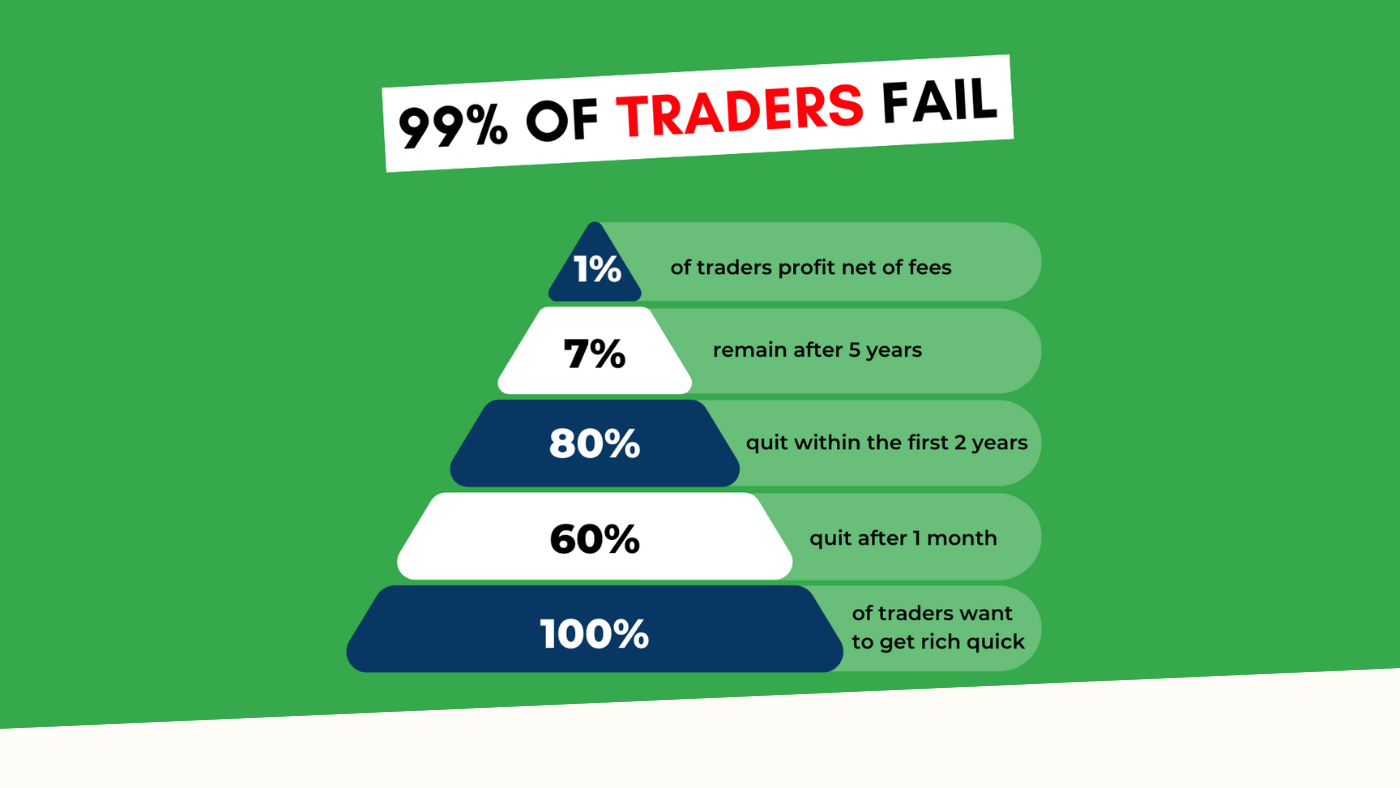

“95% of all traders fail” is the most commonly used trading related statistic around the internet. But no research paper exists that proves this...

Money management techniques describe how a trader defines the size of his trading positions. There are many different money management techniques that a trader can choose from.

The most important factor here is that the trader chooses a specific approach and does not jump around too much. Consistency in position sizing results in a much smoother account development and a trader can often avoid the wild swings that come from mismanaging position sizing.

The standard position sizing approach is called fixed percentage. Here, the trader determines the percentage level of his total account balance that he is willing to risk per single trade.

Usually, the percentage figures range between 1% and 3%. The larger the account, the lower the percentage risk usually is.

If you trade with a $10.000 account, you would risk $100 per trade if your risk level is 1%. This means that when your stop is hit, you lose $100.

The pros of the fixed percentage approach are that you give the same weight to all your trades. Thus, the account graph usually looks much smoother and has less volatility.

Disclaimer: Of course, stops don’t get always triggered and there is a substantial additional risk.

Averaging up is also known as ‘adding to a winning position’ or scaling into a trade which means that once a trade moves into profits, the trader adds more contracts to the existing position as price advances.

Pros:

Cons:

This method is often called ‘adding to losing positions’ and it is very controversially discussed among traders. It is the opposite of averaging up because once your trade moves against you, you would open new orders to increase your position size.

Pros:

Cons:

The cost averaging method is not recommended for amateur traders or for traders who lack discipline and are emotionally about their trading.

The Martingale position sizing approach is as heated discussed as the previously mentioned cost averaging method.

Basically, after a losing trade, the trader would double his position size hoping to recover losses immediately with the first winning trade because it would offset all previous losses.

Pros:

Cons:

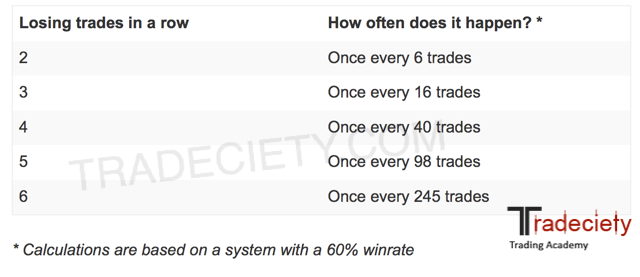

Starting with only 1% risk per trade, a trader loses his whole trading account after the 8th losing trade in a row.

| Account | % Risked | Money Risked |

| 10.000,00 | 1% | 100,00 |

| 9.900,00 | 2% | 198,00 |

| 9.702,00 | 4% | 388,08 |

| 9.313,92 | 8% | 745,11 |

| 8.568,81 | 16% | 1.371,01 |

| 7.197,80 | 32% | 2.303,30 |

| 4.894,50 | 64% | 3.132,48 |

| 1.762,02 | 128% | 2.255,39 |

| – 493,37 |

And, as statistics confirmed, losing streaks will happen no matter how good you are as a trade. Thus, it is just a matter of time until you blow up with the Martingale approach.

The anti-Martingale tries to eliminate the risks of the pure Martingale method.

With this approach, the trader does not double-up after a loss and uses his regular risk level. Therefore, a losing streak cannot wipe out the trader as fast.

On the other hand, when a trader has a winning streak, he doubles-up and risk twice as much on the next trade. The idea behind this approach is that after a winning trade, you are trading with ‘free’ money.

For example, a trader realizes a profit of $200 on his trade, where he risked 1% on a $10,000 account; now his new account size is $10,200. On his next trade, he can risk $200 which is 1.96% of $10,200. If his trade is another winner with a reward:risk ratio of 2, he makes $400 and his new account size is now $10,600. On his next trade, he can risk the $600 which are now 5.7% of $10,600.

Pros:

Cons:

The fixed ratio approach is based on the profit factor of a trader. Therefore, a trader has to determine the amount of profit that allows him to increase his position (also known as ‘Delta’).

For example, a trader can start out with trading only one contract and he chooses his Delta to be $2,000. Every time the trader realizes his profit Delta of $2,000 he can increase his position size by 1 contract.

Pros:

Cons:

The goal of the Kelly Criterion is to maximize the compounded return that can be achieved by reinvesting profits and the Kelly Criterion uses the winrate and the loss rate to determine the optimal position size. The formula looks as follows:

Position size = Winrat – ( 1- Winrate / RRR)

However, the suggested position size for the Kelly Criterion often undererstimate the impact of losses and losing streaks. Here are two examples that illustrate the point:

Example 1:

Position size = 55% – (1 – 55% / 1.5)= 25%

Example 2:

Position size = 60% – ( 1- 60% / 1) = 20%

As you can see, the suggested position sizes of the Kelly Criterion are very high and much higher than should be considered for a sound risk management. To counteract this effect, the common approach is to use a fraction of the Kelly Criterion. For example, 1/10 of the Kelly Criterion would lead to 2.5% and 2% position sizes in the example above.

Pros:

Cons:

external link:

3 min read

“95% of all traders fail” is the most commonly used trading related statistic around the internet. But no research paper exists that proves this...

3 min read

Trendlines can be great trading tools if used correctly and in this post, I am going to share three powerful trendline strategies with you.

3 min read

Choosing the right trading journal is essential for traders wanting to analyze performance, refine strategies, and improve consistency. In this...